SAPOA Update - September 2019

SAPOA Updates

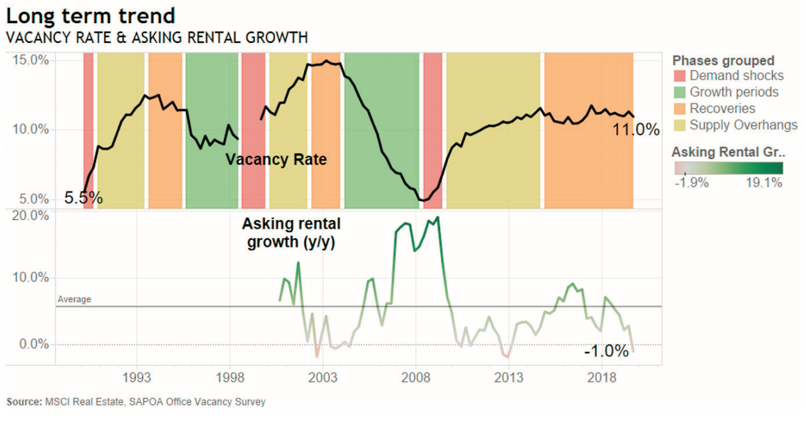

SAPOA’s latest report from September 2019 reports that, as at Q3 2019, the national office office vacancy rate in South Africa was recorded at 11.0% - a 30bp improvement compared with Q2. This improvement did, however, come at the cost of rental growth, as asking rental growth nationally declined by 1% year on year.

During the same period, 200 square kilometres of rentable area was taken up within South Africa, while 148k sqm of stock was added. The net result of this was a positive net absorption of approximately 52km sqm.

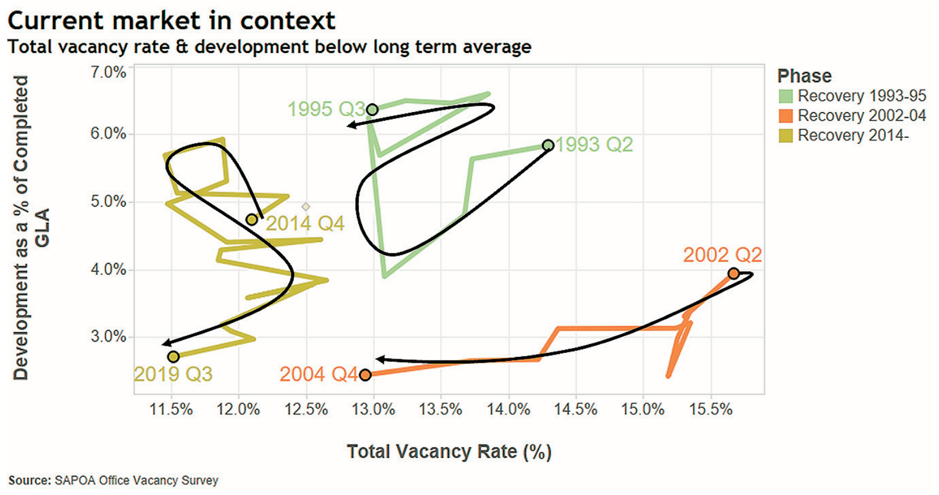

Since March 2011, SAPOA found that the total office vacancy rate (including unlet new developments) has not shifted substantially. Rather, it is trending sideways. To get down to a 5% vacancy rate will require at least 75 000 office-based new jobs – an increase of around 6.7%. This is ambitious given the currently fairly pessimistic economic growth forecasts on a broader scale.

Generally speaking, the current status of muted employment growth and low overall economy growth dampens the sector’s hopes of a short-term recovery. The current vacancy cycle is very different to the previous two in that the recovery phase is significantly more drawn out.

South Africa’s uncertainty around its credit rating, as well as the future of Eskom, means that many property occupiers are adopting a “wait and see” approach. Simon Black, founder of Black Pepper Properties, agrees, and says that the way forward is through serious structural changes to stimulate our ailing economy. "ESKOM presents the major risk to our credit sovereignty and Government needs to issue concrete reforms to ease concerns and roadmap the way forward," he says.

Since 2015, the development of new office space has been slowing down, with the demand for space growing at a slower rate. At the end of Q3, developments under construction across the country totalled only 378 sqm – the lowest levels seen since Q4 of 2005.

During Q3 ending in September 2019, vacancy rates softened in the Prime & C-grade segments but improved in the A & B-grade segments.

Given the current economic headwinds and structural growth constraints that are present in the sector, SAPOA states that it is hard to imagine a national office vacancy rate returning to mid-single digits within the next 3 years.

Generally speaking, the current status of muted employment growth and low overall economy growth dampens the sector’s hopes of a short-term recovery. The current vacancy cycle is very different to the previous two in that the recovery phase is significantly more drawn out.

South Africa’s uncertainty around its credit rating, as well as the future of Eskom, means that many property occupiers are adopting a “wait and see” approach. Simon Black, founder of Black Pepper Properties, agrees, and says that the way forward is through serious structural changes to stimulate our ailing economy. "ESKOM presents the major risk to our credit sovereignty and Government needs to issue concrete reforms to ease concerns and roadmap the way forward," he says.

Since 2015, the development of new office space has been slowing down, with the demand for space growing at a slower rate. At the end of Q3, developments under construction across the country totalled only 378 sqm – the lowest levels seen since Q4 of 2005.

During Q3 ending in September 2019, vacancy rates softened in the Prime & C-grade segments but improved in the A & B-grade segments.

Given the current economic headwinds and structural growth constraints that are present in the sector, SAPOA states that it is hard to imagine a national office vacancy rate returning to mid-single digits within the next 3 years.

Historically, 3,5% was the minimum requirement for driving employment growth, and therefore the demand for office space. However, at this point, GDP forecasts are not in this range. Therefore, SAPOA considers a national office vacancy rate in the neighbourhood of 10% as being the “new normal” for the foreseeable future. Whether or not this improves in Q4 remains to be seen.

"Ongoing tax revenue shortfalls over the past five years would indicate that increasing tax revenues have reached a logical ceiling," says Black. "A combination of strong leadership - along with difficult decisions - are required to right South Africa Inc.'s ship.

Historically, 3,5% was the minimum requirement for driving employment growth, and therefore the demand for office space. However, at this point, GDP forecasts are not in this range. Therefore, SAPOA considers a national office vacancy rate in the neighbourhood of 10% as being the “new normal” for the foreseeable future. Whether or not this improves in Q4 remains to be seen.

"Ongoing tax revenue shortfalls over the past five years would indicate that increasing tax revenues have reached a logical ceiling," says Black. "A combination of strong leadership - along with difficult decisions - are required to right South Africa Inc.'s ship.

Generally speaking, the current status of muted employment growth and low overall economy growth dampens the sector’s hopes of a short-term recovery. The current vacancy cycle is very different to the previous two in that the recovery phase is significantly more drawn out.

South Africa’s uncertainty around its credit rating, as well as the future of Eskom, means that many property occupiers are adopting a “wait and see” approach. Simon Black, founder of Black Pepper Properties, agrees, and says that the way forward is through serious structural changes to stimulate our ailing economy. "ESKOM presents the major risk to our credit sovereignty and Government needs to issue concrete reforms to ease concerns and roadmap the way forward," he says.

Since 2015, the development of new office space has been slowing down, with the demand for space growing at a slower rate. At the end of Q3, developments under construction across the country totalled only 378 sqm – the lowest levels seen since Q4 of 2005.

During Q3 ending in September 2019, vacancy rates softened in the Prime & C-grade segments but improved in the A & B-grade segments.

Given the current economic headwinds and structural growth constraints that are present in the sector, SAPOA states that it is hard to imagine a national office vacancy rate returning to mid-single digits within the next 3 years.

Historically, 3,5% was the minimum requirement for driving employment growth, and therefore the demand for office space. However, at this point, GDP forecasts are not in this range. Therefore, SAPOA considers a national office vacancy rate in the neighbourhood of 10% as being the “new normal” for the foreseeable future. Whether or not this improves in Q4 remains to be seen.

"Ongoing tax revenue shortfalls over the past five years would indicate that increasing tax revenues have reached a logical ceiling," says Black. "A combination of strong leadership - along with difficult decisions - are required to right South Africa Inc.'s ship.Related blog posts (4)

Covid-19: Can you get rent relief on your commercial property?

Commercial Property

Benefits to Leasing Commercial Property

Property Insights

Finding commercial space for your business

Property Insights